When we think of wind energy, we picture the production of clean, zero-emission energy. However, as with any major technological transition, there is a downside we must begin to address: the end-of-life management of wind turbines.

The figures speak for themselves: Europe is bracing itself for a wave of wind turbines to be disposed of or refurbished. Let’s take a look at what is happening and why ‘circularity’ is the sector’s next real challenge.

Unstoppable growth

According to the decarbonisation scenarios outlined by the European Commission, wind energy is set to become the cornerstone of our continent’s energy system. The aim is to reach up to 1,300 GW of installed capacity by 2050.

This exponential growth brings with it an inevitable consequence: a staggering increase in demand for raw materials. To build the permanent magnets for these new-generation super-turbines, we will need ever-increasing quantities of critical materials, particularly rare-earth elements. A precious resource, complex to extract and geographically concentrated.

The ‘retirement’ of the first turbines: the figures

The first generations of European wind farms are ageing. In 2022, the average age of turbines in the European Union was 13.7 years, compared to an estimated operational lifespan of between 20 and 25 years.

The time to act is now, because the end-of-life figures are already significant:

- The historic wind farm. Turbines totalling around 14.2 GW (representing 8% of installed capacity but as much as 20% of the total number of existing turbines) are already over 20 years old. They will soon need to be decommissioned or undergo repowering (i.e. replacement with more modern and efficient models).

- The looming deadline. Around 38 GW of onshore wind capacity has already reached or is reaching the end of its operational life in the coming years, between 2021 and 2025.

The crucial issue: the mountain of waste on the way

Whilst components such as the steel and copper in the towers are easily recyclable, the real industrial and environmental challenge lies with the blades, often made of composite materials (glass or carbon fibre bonded with resins) which have historically been difficult to separate and reuse.

The challenge for the future is to transform this mountain of waste into a goldmine of resources. Developing advanced recycling technologies for the blades and recovery chains for rare earths is no longer just an ecological choice, but an economic necessity to ensure Europe’s energy and strategic independence.

Repowering: the future of European wind power

The wind energy sector in Europe is entering a new phase of maturity in recent years. It is no longer just a matter of identifying new sites and installing wind turbines where there were none before, but of optimising what already exists. The continent’s first wind farms are in fact reaching the end of their operational lifespans , opening the door to one of the greatest industrial opportunities of the energy transition: repowering.

The latest data on the European market points to a very clear path: the road to sustainability lies in technological upgrading.

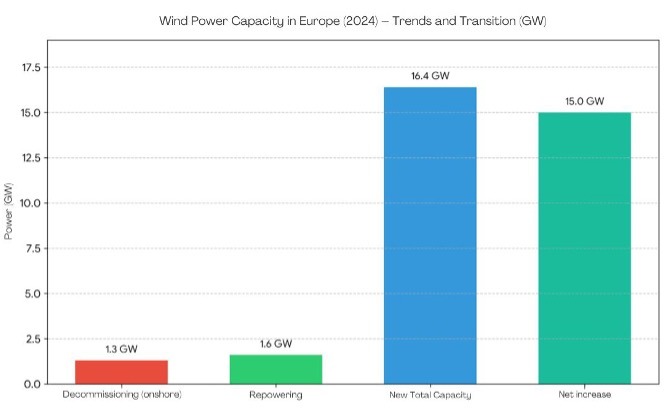

The numbers behind the change: the 2024 review

2024 was a pivotal year for understanding the dynamics between the decommissioning of old plants and the emergence of new ones. Europe saw a sharp acceleration in this technological transition:

- 1.3 GW of old wind capacity was decommissioned, spread across 8 key countries (Germany, Spain, Italy, the Netherlands, Austria, Sweden, France and the United Kingdom). All decommissioning involved onshore plants (on land).

- New impetus from repowering. At the same time,6 GW of capacity was installed specifically from repowering projects (out of a total of 16.4 GW of new annual installations).

- Overall growth. Thanks to the combined contribution of new wind farms and repowered plants, the net increase in European capacity was 15 GW.

Data analysis in brief

- Repowering takes the lead: With6 GW of repowered plants compared to 1.3 GW of decommissioned capacity, Europe has managed to fully offset the decommissioned onshore capacity, even generating a ‘surplus’ of power (+0.3 GW) by using less space or more efficient wind turbines.

- New capacity vs net increase: Of the 16.4 GW of total new installations, the actual net increase is 15 GW. This precise difference represents the old capacity that has been permanently shut down or replaced to make way for the new generation of turbines.

The map of decommissioning and repowering

Not all countries are progressing at the same pace. Germany remains the undisputed driving force behind this transition: it alone led decommissioning with 712 MW (over half the European total) and topped the repowering rankings with a substantial 1.1 GW installed.

Alongside Germany and Italy (which recorded 155 MW of repowered capacity), Spain also forms part of the trio accounting for over 90% of the decommissioned capacity on the continent, although Madrid did not install any new repowered capacity during the year.

The perfect equation: tripling output with 25% fewer turbines

Why is repowering considered such a brilliant strategic move? The answer lies in an extraordinary efficiency figure: repowering allows energy production to be tripled on average whilst reducing the number of turbines by 25%.

New-generation turbines are radically more efficient and powerful than those installed twenty years ago. Replacing four old wind turbines with three modern models not only improves the visual impact on the landscape but also increases the amount of clean electricity fed into the grid.

The 4 competitive advantages of repowering

Choosing to repower an existing site rather than developing one from scratch offers enormous benefits to developers and local communities:

- Wind resource already certified. Existing sites are already located in the areas with the best wind conditions.

- Historical operational data. Operators have years of real-world data on production and wind behaviour in that specific area, reducing estimation risks to zero.

- Infrastructure already in place. Access roads, grid connections and substations are already in place and operational, drastically reducing capital expenditure (Capex) and construction times.

- Less local opposition. As local communities are already accustomed to the presence of the wind farm (which, incidentally, will see a reduction in the number of turbines), social acceptance of the project is significantly higher, reducing red tape and objections.

The 2025–2030 outlook: what lies ahead in the coming years

The wave of renewal is only just beginning. Looking ahead to the second half of the decade, the European roadmap envisages a major overhaul of the wind farm fleet:

- 22 GW of total capacity will be decommissioned.

- 12 GW of this will be repowered (thanks to the efficiency of the new turbines, this will generate a total of 26 GW of repowered capacity).

- The remaining 10 GW that have reached the end of their life will be completely removed, restoring the land to its original state.

Compton Industriale is well aware that the future of wind energy depends not only on the installation of new turbines, but also on the ability to recover and repurpose existing ones. In light of the data presented in this article, it is clear that the recycling of wind turbine blades represents a crucial investment for Europe over the next decade: our company is committed to playing a leading role in supporting the energy transition and strengthening the circular economy.